There are many ways you can pay your home loan off faster, use an offset account, paying fortnightly or paying a little extra. No matter how you add it all up, it will make a bit of difference, but nothing too dramatic.

But imagine if you could pay off your mortgage 10, 12, 14 or even 18 years sooner; what a game-changer that would be. Imagine having no mortgage 10 whole years sooner than expected. How much would that change your life?

The day you’re free of personal debt is a great one for many reasons. It’s an achievement worth celebrating for the years of hard work that helped you reach that goal.

I have created a program that shows you how you can be debt-free a decade or more faster than you are tracking right now.

It’s called Mortgage Eliminator, and as a reader of our Better Homes and Gardens Real Estate blog, you can order a copy of this report based on your situation with our compliments.

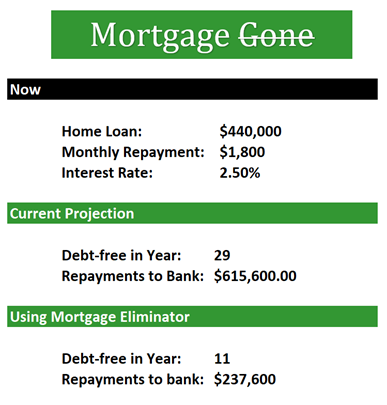

Let’s look at how it works; Sandeep and Kiara have a $440,000 home loan, based on their current payments, they will be debt-free in 29 years. The Mortgage Gone strategy shows them how they can eliminate their mortgage in just 11.

No home loan 18 years faster, 18 years of not paying a $1,800 a month mortgage, 18 years to use that money in other ways.

Let’s see how it works.

The premise is simple but effective and low risk. They buy a low-risk investment property.

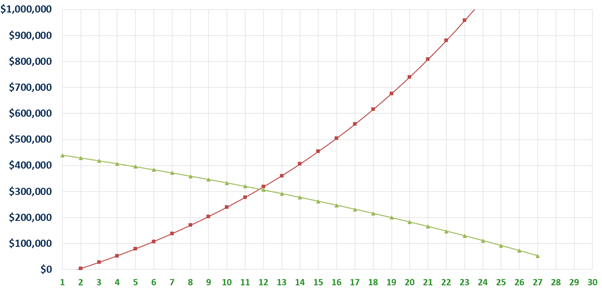

When you have a home loan and buy an investment property, you have two lines moving towards each other.

One line is going down (the balance of your home loan, as you pay it off). The other is going up (the value of your investment property). One day the lines will meet. When they do, you’ll be able to sell your investment property, pay the capital gains tax and selling costs, and the profit will pay off your home loan in full.

Like this:

ELIMINATE YOUR PERSONAL DEBT TIPPING POINT

Too good to be true? Well, it’s not. This can be done quickly and safely, but you must get some of the fundamentals right, and they are:

- Buying a low-risk investment property, the type that has a long track record of success.

- Selecting a property with cash flow so good it will pay for itself.

- Choosing a homeowner quality investment property situated in a good location that will achieve consistent capital growth.

And that is where we can assist you. We have been helping our clients buy properties just like those for over 20 years.

In the following example, we have used an investment property value of $500,000 and a capital growth rate of 6%.

6% capital growth means the property will double in value every 12 . (You can judge from your own experience) But what if the property Sandeep and Kiara buy only get half of that, just 3% capital growth? They can still be debt-free in just 17 years, 12 years faster than they otherwise would.

By the way, when you own several investment properties, one will often grow in value more quickly than the others; it doesn’t matter which one you sell to be personally debt-free.

If one gives you better than average capital growth, you might be reluctant to sell, even to pay off your home loan, but there’s no guarantee it will perform just as well in the next 10 years.

Do you have to wait until you can wipe off your total home loan in one go? No, you don’t. I remember a couple I worked with, Bill and Margaret, who were keen property investors with a large home loan and a plan. As soon as one of their investment properties showed a decent capital gain, they would sell it and pay a lump sum off their home loan. They kept this up until they were debt-free, then they sold up and bought a farm. It took about 10 years, but they were debt-free, 15 years ahead of schedule.

Would you like a free report showing you when you can be debt-free on your home?

Simply email the following information to info.melbourneinvest@bhgre.com.au

- Your contact details

- Your home loan balance

- The interest rate on your mortgage

- Your monthly payment

We will be back to your own personalised report in a few days, and you will see what impact this strategy will make to your personal financial future.

If you have any questions about this strategy or anything to do with property investing, email us, and we will get back to you.

Author: Michael Sloan

Managing Director of Better Homes and Gardens Real Estate Melbourne Invest and author of ‘The Formula to Successful Property Investing’

Disclaimer: The opinions posted within this blog are those of the writer and do not necessarily reflect the views of Better Homes and Gardens® Real Estate, others employed by Better Homes and Gardens® Real Estate or the organisations with which the network is affiliated. The author takes full responsibility for his opinions and does not hold Better Homes and Gardens® Real Estate or any third party responsible for anything in the posted content. The author freely admits that his views may not be the same as those of his colleagues, or third parties associated with the Better Homes and Gardens® Real Estate network.